By Professor em. Samuele Furfari, a former longtime senior official at the Energy Directorate-General of the European Commission, and Professor em. Alain Préat:

The United States have been self-sufficient when it comes to energy production for several years now, mainly thanks to shale gas, whose price is 15 times less than the gas price in the European Union (EU), and which is produced in very small quantities. Russia has nearly 200 trillion cubic meters of natural gas, making it the world’s largest proven natural gas reserve (20%), ahead of Iran and Qatar, as it is also the world’s largest gas exporter.

The United States, only in 2016 still a net importer of gas, have become one of the world’s leading exporters of LNG, in the space of a few years. In 2021, the United States exported 100 billion m³ (Gm³) of LNG (= Liquefied Natural Gas, transported by ship in liquid form at a temperature of -161°C). As Russia is only able to export gas to two regions (Europe and Asia), due to the distribution networks of the pipelines, it has dealt with this by taking away the export monopoly from its gas giant – Gazprom – to start exporting LNG as well.

Currently, Gazprom produces about 550 bcm of gas per year, plus another 100 bcm produced by independent Russian producers, or imported from Central Asia, which makes up for a total annual volume of over 650 bcm. Almost two thirds of that is used for domestic consumption, while 75 Gm³ is exported to the countries of the former USSR and around 150 Gm³ to other countries, mainly to the European Union (graph 1).

The European Union depends on Russia for 45.3% of its gas supply (as announced by European Commission on 8 March 2021, as opposed to the often cited figure of 40%), Norway for 23.6% and Africa (Nigeria, Algeria, Libya) for more than 10%, with the remainder coming from the United States and the Middle East, particularly Qatar.

Most Russian gas is distributed to Europe through three major continental pipelines (Nord Stream 1 across the Baltic Sea, Yamal-Europe through Belarus and Poland, and Brotherhood through Ukraine). Nord Stream 1, which has a capacity of 55 Gm³/year, was supposed to be duplicated by a fourth with the same capacity, Nord Stream 2, financed by Gazprom (Russia) and German companies (BASF, Wintershall), as well as by Engie and Shell. It has been completed and was due to enter service following a routine administrative procedure in 2022, but following the war in Ukraine, the German government decided to suspend its certification.

Gas accounts for about a quarter of the European Union’s energy consumption. It is mainly used for domestic and industrial heating (70%) or to generate electricity (30%).

Although some EU Member States produce gas themselves, like the Netherlands and Romania, this production is too small to cover the needs of all households and businesses in the EU. The European Union must therefore look elsewhere for this energy, especially to Russia (around 150 to 170 Gm³ depending on the severity of the winter).

The EU remains by far the leading export destination for Russian gas (78% of exports). Russia’s energy strategy for the EU has mainly consisted in increasing its exports to the EU.

What would an EU embargo on Russian gas entail?

An embargo on Russian gas to the EU would mean that Russia’s gas profits would be strongly reduced as all of its pipeline gas exports go to the EU. This would leave them with only exports to LNG terminals in Asia (China, Japan, Korea and Taiwan).

Since Middle Eastern countries have LNG delivery contracts with Asian countries, the only credible substitute for the EU is LNG from the US, provided that the Biden Administration stops its harassment of shale gas producers, following promises made during Biden’s election campaign.

All that would be needed are ports equipped to receive LNG tankers and to regasify the LNG. In Europe, many ports are equipped (Belgium with Zeebrugge, Holland, France, Spain, Lithuania, etc.), but strangely Germany, although it is the largest economy in the EU, has none, due to German ecologists being strongly and firmly opposed to this “safety valve”. Once regasified in European ports, that gas can be redistributed anywhere in the EU, through an interconnected network of pipelines.

A closer look at the LNG market

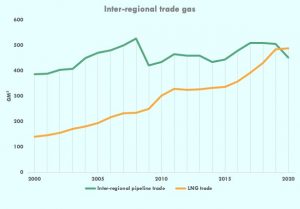

The global LNG market in 2020 was 490 bcm, or 12.3% of global natural gas consumption and 2.6% of primary energy consumption. More than half of the GLN (50.9%) is exported, the rest (48.1%) is delivered regionally (inter-regional pipelines, here).

The graph below shows how important LNG has become in world gas trade over the last 20 years:

The Global LNG trade is thus expected to more than double by 2040 to 729 bcm (even more than current pipeline trade). The share of LNG in world gas trade would then be nearly 60% (Source: Iris-France).

The main LNG exporting producers are Australia (21.8%), Qatar (21.7%), USA (12.6%), Russia (8.3%), Malaysia (6.7%) and Nigeria (5.8%) (Source). 60% to 70% of their supplies go to South East Asia (especially China, Japan and Korea. These three countries account for 50% of global demand) and 21% go to the EU.

To do without Russian gas, 160 Gm³ would have to be transferred from South East Asia to the EU, which would mean cutting South East Asian gas consumption with 50%. That is Impossible!

*Not Enough LNG to Fuel EU‘s Shift From Russian Gas – BBG

I fear that no one really thought this through. pic.twitter.com/6k25fjh00m

— Fabian Wintersberger (@f_wintersberger) March 15, 2022

Unlike gas pipelines, LNG tankers head where the market decides, on the basis of demand, to the highest bidder, which will generate competition between the EU and Asia, with higher prices.

In this context, China, which has 28 gas terminals, could very well buy Russian LNG (especially from Sakhalin, i.e. in Asia) at a discount and sell it to the EU at a high price, since China has no major energy problem since it has no concerns to take advantage of its own abundant and cheap coal.

In the Climate Agreement of the COP21 in Paris (2015), China (and India) have taken advantage of the situation in a clever way, committing to gradually reduce coal exploitation only from 2030 on and without giving a date for the final abandonment, contrary to the EU countries which, after having drastically reduced the exploitation of this resource, are also eliminating its consumption. The new German government in particular has planned to bring forward the date of finally abandoning coal consumption, which was negotiated by Angela Merkel, from 2038 to 2030). It would therefore be a good financial deal for China to replace gas with coal.

An embargo on Russian gas would furthermore slow down the activity of Gazprom, Rosneft, due to the shutting down of production wells etc. This would cause global supply to ultimately decrease, while prices would increase accordingly.

At the root of the problem: The EU’s promotion of renewable energy

The European Union’s energy policy of promoting renewable energies since 2005, with Angela Merkel’s Road Map, called the “energy transition”, has led to the subjugation of the EU to a very dominant supplier, Russia, and to a single product, gas.

This is most strikingly the case for Germany, which has abolished its nuclear power plants and is preparing to do the same for its cheap lignite power stations, in a bid to promote very expensive so-called intermittent renewable energy, in the name of ecology.

Give how this does not work – there is not always enough wind for wind power, nor is there always sufficient sun for solar panels, etc. – Germany has recently had to build new gas-fired power stations. Faced with this energy ‘disaster’ (which a mere look at one’s recent electricity and heating bill will confirm), many countries are reviving their nuclear power plants, including Belgium.

Is renewable energy a failure? Yes. in January 2022 it only produced a little less than 2% of electricity at peak times.

It must be stressed, this situation was predictable. In October 2000, the European Commission published a Green Paper on the security of energy supply in the EU. It defined a common sense strategy which consists in not putting all the eggs in the same basket:

First, diversify the types of primary energy used. Secondly, it is prudent to diversify the countries from which this energy is imported and thirdly, even for the same energy and the same country, it is wise to diversify the routes and means of supply.

“The EU has ignored its own strategy to diversify energy supply”- Interview with Prof. Samuele Furfari @furfarisamuele, a former longtime senior official at the Energy Directorate-General of the European Commission:https://t.co/Ap99IPB3TV Interview conducted by @EuropeScientist

— BrusselsReport.EU (@brussels_report) March 21, 2022

Germany is a perfect example of the mistaken European energy policies: it is excessively dependent, not on natural gas (it only accounts for 36%), but on Russian gas. In 2019 it imported 84 Gm³, of which 51 Gm³ came from Russia.

Moreover, a second mistake for such an important economy was for Germany not to build a single gas terminal to receive LNG carriers carrying liquefied natural gas (LNG) to supply the world market. Environmentalists opposed the various projects presented, seeing them as perpetuating the import of fossil fuel.

The definitive view on (1) dependence on gas in EU countries' energy mix, and (2) dependence on Russia for gas.

German reluctance to cut Russian gas instantly clear – it is among the most dependent on gas in its energy mix with almost 60% of the gas coming from Russia. https://t.co/C7WNRseqHb pic.twitter.com/WL39Yc8OXA

— Daniel Kral (@DanielKral1) April 4, 2022

🇩🇪 – Can Germany cope without Russian gas?

• Government says no and economists say economic impact would be only minimal

• Answer depends on whether we're talking about short-term (hard to do) or long-term (doable)

• In long term lower dependency on Russian energy unavoidable pic.twitter.com/98pfWWIqSR— Agathe Demarais (@AgatheDemarais) April 19, 2022

What’s the solution?

Now how do we get out of this crisis and square the circle?

The supply in the near future (during 2022) of 15 Gm³ of LNG from the United States will reduce the European Union’s dependence on Russia by 8%, from 44% to 36%, while our ‘dependence’ on the United States will increase from 7% to 15%. The EU now plans to push this up to 50 Gm³ of US LNG by 2030.

It is useful to remind that the EU has encouraged Member States to oppose the exploration – let alone the exploitation – of shale gas. Now, they are begging the US to supply it. Has it suddenly become less polluting?

Bavarian premier calls for German shale solution – https://t.co/L8zL86iSKu – NGW News & Insight

— Natural Gas World (@NatGasWorld) April 11, 2022

By sourcing gas elsewhere in the medium term (Africa and others, including Norway and Qatar), the EU’s dependence on Russia could be reduced by 25%.

Finally, since natural gas is mainly used for heating, a reduction in heating thermostats could contribute to a further 10% reduction compared to Russia.

These scenarios are subject to strong uncertainties as long as regasification infrastructures are not further developed. Indeed, Europe lacks structures to unload cargoes from ships into the pipeline network, and it lacks storage sites and interconnections. This is hardly surprising, since for years, fossil fuels have been castigated, while renewable energies have been promoted. How can we expect investors to invest in the missing infrastructures when the European Commission keeps repeating that we must abandon fossil fuels?

It should be remembered that liquid methane regasification terminals are very expensive to build, costing generally one billion euros per terminal, and take almost two years to complete. Most of the current terminals are already saturated, and in this context the Zeebrugge terminal, an asset for Belgium, will be expanded between now and 2024.

The aim is for Europe to be completely free of Russian gas by 2027. In the meantime, Europe will also draw on 80% of its strategic stocks to get through the winter of 2022-2023.

The EU and Russia are at risk of triggering a de facto embargo on Russian gas https://t.co/kClH72BFr7

— Bloomberg Asia (@BloombergAsia) April 16, 2022

"According to an admittedly ambitious plan from RePlanet called Switch Off Putin: Ukraine Energy Solidarity Plan, by simply reversing the nuclear phase-out underway in Germany, Sweden, and Belgium, Europe can offset 1.4 bcf/d of Russian gas (or approximately 10% of the gap)."

— Pieter Cleppe (@pietercleppe) April 14, 2022

Originally published in French by the Science, climat et énergie blog

Disclaimer: www.BrusselsReport.eu will under no circumstance be held legally responsible or liable for the content of any article appearing on the website, as only the author of an article is legally responsible for that, also in accordance with the terms of use.