By Dyuti Pandya and Vanika Sharma, analyst and economist at the European Centre for International Political Economy (ECIPE)

India’s premier, Narendra Modi, has just finished a tour in Europe, visiting several capitals to build stronger commercial relations. In late January this year, India and the European Union finished negotiations for their new trade agreement, billed as the ‘Mother of All Deals’. While that may be an exaggeration, the phrase captures the scale and political ambition of the agreement, marking a major step forward in an emerging but increasingly significant trade partnership. The agreement seeks to reshape the EU–India trade through more predictable regulatory procedures, improved market-access provisions and deeper supply-chain linkages. While lower tariffs reduce transaction costs, additional provisions can lower compliance burdens and create new commercial opportunities.

The timing of the agreement is also significant. It comes at a critical time for both countries, amid rising uncertainty in traditional trade alliances, growing interest in supply chain diversification and shifting global trade priorities. While the FTA reflects a strategic push toward deeper global integration for both regions, it also sits within a wider EU–India economic partnership, including frameworks such as the EU–India Trade and Technology Council (TTC) and the EU–India InnoCenter, which support cooperation in areas such as strategic technologies, innovation, resilient supply chains and startup collaboration. In this sense, the agreement can be interpreted not simply as traditional tariff-led liberalisation but as a more flexible form of trade cooperation aimed at supporting diversification and strengthening economic resilience against the backdrop of ongoing geopolitical and economic uncertainty.

Seen in this context, the FTA offers significant scope to broaden EU–India economic partnership. For the EU, the agreement could offer improved access to a large but still highly protected Indian market. For India, it provides an opportunity to improve competitiveness in the EU market, diversify exports and strengthen integration into global value chains. However, the success of the FTA will depend on how well it complements the existing comparative advantages of both regions and if they are able to capitalise on emerging opportunities in trade. This blog examines the existing and emerging trade relations between the EU and India and assesses the potential benefits of the agreement for both regions in an increasingly unpredictable global economy.

A Window of Opportunity

In 2024, the EU was India’s second largest trading partner after China, accounting for 11 per cent of India’s total global trade. Meanwhile, India was the EU’s tenth largest trading partner, accounting for 1.7 per cent of EU’s global trade abroad. This reflects an asymmetry in the weight each partner carries in the other’s overall trade profile: the EU is a major market for India, while India remains a relatively smaller, though increasingly relevant, partner for the EU.

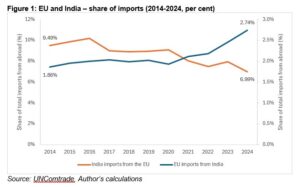

This asymmetry is also visible in the way the trade relationship has evolved over time. Figure 1 shows the share of EU imports from India as a share of EU’s total imports from abroad and the share of Indian imports from the EU as a share of India’s total imports from abroad between 2014 and 2024. While India’s importance as a market for the EU has seen a decrease over time, the EU market has become more important for India. Particularly, since 2020, there has been a sharp increase in the share of India’s exports to the EU. Between 2020 and 2021, this trade expansion can be explained by the increase in India’s exports of pharmaceutical products against the Covid-19 pandemic. However, the persistent upward trend post 2021, including an even sharper increase in 2023, could signal more trade openness from India and increasing diversification from the EU.

Meanwhile, the share of India’s imports originating from the EU has declined over the same period, suggesting a gradual shift in India’s relative sourcing patterns. This does not necessarily imply a reduction in absolute imports from the EU, but rather that India’s imports from other regions may have expanded more rapidly. In particular, India’s import basket appears increasingly oriented toward Asian and Indo-Pacific suppliers, including Northeast Asia, ASEAN, and West Asia/ Gulf Cooperation Council (GCC), reflecting the role of regional production networks and cost-competitive manufacturing ecosystems. The observed decline in the EU’s import share is therefore better interpreted as a relative diversification of India’s import base and deeper integration into global and regional value chains, rather than as evidence of disengagement from European suppliers.

These trends point to a clear imbalance but also to a window of opportunity. India’s role in EU imports has grown, yet it still accounts for only a small share of the EU’s overall import basket. Similarly, while the EU remains a major trade partner for India, its relative position in India’s import market has weakened. The EU-India FTA could, therefore, help address both sides of this gap: by supporting stronger Indian export growth to the EU, while also improving market access for EU firms in India.

For instance, based on the memo for the EU-India FTA, India has committed to eliminating tariffs on 86 per cent of tariff lines, covering 93 per cent of the trade value, creating immense opportunities for increased EU exports to India. The economic value of exporting more to India doesn’t stop there. Presenting a market of close to 1.5 billion people, with an expanding middle class, India offers the EU an important source of export diversification and long-term demand growth.

For India, the agreement offers an equally important opportunity. In 2024, India was the eighth largest supplier to the EU, accounting for only 3 per cent of EU’s imports from abroad. As a large economy, abundant with labour and capital, these numbers represent an underutilised export potential. Under the EU-India FTA, the EU has committed to eliminating tariffs on over 90 per cent of tariff lines, representing 91 per cent of the trade value, presenting a window for India to drive export growth and increase its share in EU imports. This would give Indian exporters improved access to one of the world’s largest markets and could help India increase its share in EU imports over time.

Taking a Closer Look

The changing structure of EU-India trade suggests that the relationship is no longer concentrated mainly in traditional or lower-value goods. Over the past decade, trade between the two partners has shifted increasingly toward higher value-added sectors.

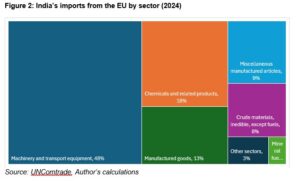

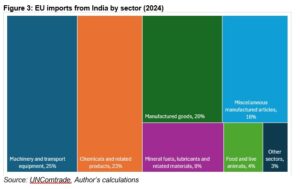

Between 2014 and 2024, EU’s imports from India of food and live animals decreased from 7 per cent to 4 per cent, meanwhile, the share of machinery and transport equipment sector has increased from 15 per cent to 25 per cent and that of chemicals has increased from 16 per cent to 23 per cent. On the other hand, between 2014 and 2024, India’s imports from the EU of manufactured goods have decreased from 34 per cent to 13 per cent, while imports of machinery and transport equipment saw an increase of 32 per cent to 48 per cent. In 2024, for both India and the EU, the largest imports from each other were in the machinery and transport equipment, chemicals, and manufactured goods sectors.

Figure 2 shows that these three sectors accounted for 79 per cent of India’s total imports from the EU in 2024. These are also the same sectors where the EU stands to benefit from the trade deal. In particular, tariffs on cars will fall sharply from 110 per cent to 10 per cent, while high tariffs of up to 44 per cent on machinery, 22 per cent on chemicals, and 11 per cent on pharmaceuticals will be largely eliminated.

This represents a substantial reduction in market entry costs for EU exporters, making their products significantly more price-competitive in India. As a result, EU firms in these sectors could expand their market share, particularly in capital goods and high-technology products where demand is less price-sensitive but previously constrained by prohibitive tariffs. The sharp tariff cuts on automobiles are especially significant, as they transform what was effectively a closed market into a commercially viable one for EU producers. Overall, this will potentially deepen EU penetration in high-value sectors and also increase India’s access to advanced technologies and industrial inputs.

Although EU goods are generally more expensive, the very high tariffs previously in place more than doubled their prices, effectively pricing them out of the Indian market. Tariff reductions will make EU products commercially viable for firms and higher-income consumers who prioritise quality, reliability, and advanced features over cost. This is particularly relevant for capital goods such as machinery and specialised chemicals, where performance and efficiency matter more than price alone. And more Indian firms may be able to afford importing these inputs, enabling them to upgrade their own production process and produce higher quality goods.

Figure 3 shows EU imports from India by sector in 2024. The data indicate that India’s exports to the EU remain concentrated in three main sectors: machinery and transport equipment, chemicals, and manufactured goods. This matters because the FTA is unlikely to affect all sectors in the same way. In these higher value-added sectors, tariff cuts may help, but competitiveness also depends on standards compliance, certification, reliability, technology intensity and established buyer relationships. The agreement can support these sectors by lowering trade costs and improving predictability, but the gains are likely be gradual and concentrated among firms that are already export-ready.

The more immediate export gains may come from sectors where price competitiveness plays a larger role. In labour-intensive and MSME-linked industries, buyers are often sensitive to small differences in landed prices, and Indian exporters compete directly with suppliers from economies such as China, Bangladesh and Vietnam. Tariff preferences under the FTA could therefore help narrow this competitiveness gap, particularly in sectors such as textiles, leather and footwear, tea, coffee, spices, sports goods, toys, gems and jewellery, processed foods and selected marine products.

The agreement creates these opportunities through different forms of market access. Some products are expected to move toward zero-duty access within three to five years, including processed foods and selected marine products. Others will benefit from preferential tariff reductions, such as poultry products, preserved vegetables and bakery items, while certain products, including shrimp and prawn products, will receive access through tariff-rate quotas. The key point is that these provisions reduce the tariff disadvantage faced by Indian exporters in sectors where even small price differences can affect market share.

This is especially relevant for textiles and apparel. Indian exporters have historically faced a tariff disadvantage in the EU compared with competitors such as Bangladesh, Pakistan and Turkey, which benefit from preferential access to the European market. The FTA helps correct this gap by improving India’s tariff treatment in a large EU textile and apparel market. This could support export diversification while also strengthening one of India’s most employment-intensive sectors, which is closely linked to MSME clusters and regional production networks.

The EU is India’s second-largest export destination for textiles and apparel after the US, while the EU’s global textile and apparel imports stood at USD 263.5 billion in 2024. By contrast, India’s textile exports to the EU were around USD 7.2 billion, suggesting significant room for expansion if tariff preferences allow Indian firms to compete more effectively. The potential gains are therefore not only commercial but also developmental, given the sector’s role in employment generation and small-firm participation.

Special Commitments – Trade in Services

The EU-India FTA provides specific commitments on trade in services between the two regions. This is particularly important given the changing nature of trade with the advent of digital technologies, trade in human capital, and increasing exchange of ideas and knowledge. This is particularly relevant for India, whose comparative strength in ICT and business services gives services trade a central role in its economic relationship with the EU.

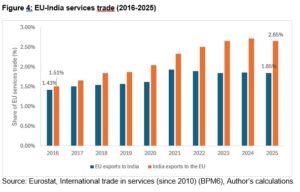

Figure 4 shows EU exports of services to India as a share of total exports abroad and EU imports of services from India as a share of total imports from abroad. Both shares have increased over time, with the share of Indian exports to the EU claiming a larger percentage than EU exports to India.

In 2024, India’s largest services exports to the EU were other business services (€21.3 billion), ICT services (€12.9 billion), and transport services (€3.8 billion). Meanwhile, the EU’s largest exports to India in 2024 were also in the same three sectors amounting to €9.5 billion in the ICT sector, €9.3 billion in the transport services, and €6.1 billion in other business services. This overlap matters because it shows that services trade between India and the EU is not marginal to the relationship; it is increasingly concentrated in sectors that support digital trade, logistics, professional activity and wider business integration.

Services trade becomes a central element of the EU-India FTA, reflecting the importance of the sector in both economies. The agreement provides substantial sectoral coverage through specific commitments (Chapter 8 of the FTA). For instance, India has secured commercially meaningful EU commitments in around 144 sectors and sub-sectors, including computer-related services, IT/ITeS, professional services, other business services and education services. In return, India has provided commitments across 102 sectors and sub-sectors of EU interest, including maritime transport, financial services, telecommunications and environmental services.

For India, the most significant opportunities may arise in ICT, IT/ITeS, other business services and professional services such as architecture and engineering. These are sectors where India already has export strengths and where demand could grow as firms rely more heavily on digitally delivered services, remote business support and specialised professional expertise. The agreement could also support the expansion of Global Capability Centres in India by improving predictability for cross-border services supply and strengthening links between Indian service providers and European clients.

In transport services, the expected benefits may be more mixed. India has preserved policy space in areas such as domestic coastal shipping, which limits the extent of liberalisation in this segment. However, the agreement can still create opportunities through commitments in maritime transport and related auxiliary services. Improvements in shipping, logistics, freight forwarding, storage and port-linked services could support goods exporters by reducing trade frictions and strengthening connectivity between Indian and European markets.

The services provisions should nevertheless be read with some caution. Although they create new commercial openings, conditions, such as the movement of professionals and the governance of cross-border data flows, needed for services trade to expand smoothly are not fully resolved within the FTA. The services chapter, therefore, represents a meaningful opening, but not full liberalisation. It can create opportunities in sectors where India and the EU already have strong commercial links, especially ICT, business services, professional services, transport, telecommunications and financial services. In this sense, the services provisions reinforce the wider logic of the FTA: the agreement is not only about expanding goods trade, but about widening the scope of EU–India economic cooperation across sectors where both sides have existing strengths and future growth potential.

Conclusion

The EU-India FTA comes at a critical time for both economies, offering an opportunity to deepen economic cooperation amid growing global uncertainty and shifting trade relationships. By reducing barriers across goods and services, the agreement can help the EU diversify its partnerships and strengthen its presence in one of the world’s fastest-growing markets, while enabling India to expand exports, attract investment, upgrade industries and integrate more deeply into global value chains.

The analysis shows that the FTA’s potential lies in how it responds to different but complementary needs on both sides. For the EU, the agreement offers a chance to regain ground in the Indian market, particularly in high value-added sectors where tariffs have limited commercial viability. For India, it offers an opportunity to improve competitiveness in the EU market, especially in labour-intensive and MSME-linked sectors where preference disadvantages have constrained export growth. At the same time, the agreement reflects the broader shift in EU-India trade, which is no longer limited to traditional goods but is increasingly shaped by high value-added goods and services.

The agreement offers a combination of scale, complementarity and unrealised potential, creating a clear framework for building a more balanced, diversified and commercially meaningful EU-India economic partnership.

Disclaimer: www.BrusselsReport.eu will under no circumstance be held legally responsible or liable for the content of any article appearing on the website, as only the author of an article is legally responsible for that, also in accordance with the terms of use.

")