International tax-rate competition is being replaced with rigid centralization, which is setting the stage for higher taxes in the future, experts warn in a new publication for Geopolitical Intelligence Services (GIS). This latest GIS document chronicles how the Organisation for Economic Co-operation and Development (OECD), the European Commission and the U.S. administration of President Joe Biden have been working in lockstep to upend the system for taxing corporate profits. The existing international rules, the GIS authors note, are being replaced with a stiff, centralized scheme aimed at eliminating tax competition.

The authors of the new paper are Adam N. Michel, Ph.D., the director of tax policy studies at the Cato Institute and Enrico Colombatto, University of Turin economics professor and director of research at the Institut de Recherches Economiques et Fiscales (IREF) in Paris. They have been studying this regulatory revolution as it evolved and morphed over the years. Commenting on the new study, Prince Michael of Liechtenstein, GIS founder and commentator, sounds the alarm that centralization and bureaucratic overregulation pose a threat to a democratic, free and prosperous Europe.

The Two-Pillar solution, first outlined by the OECD in October 2020 and since endorsed by some 140 countries (or, more precisely, their executive branches), aims to ramp up the taxation of multinational businesses by hiking effective tax rates and moving taxing rights away from a few countries and granting them to many others. The rationale for the change is based on allegations that international corporations would have been abusing the existing system to avoid paying their fair share in taxes. The GIS publication however shows that hard statistical data contradict this claim. Despite this, it remains popular with politicians and the general public.

Pillar One aims to change where some companies pay taxes, selectively moving toward a system based on customer location instead of business activities. Pillar Two includes a series of new rules that would enforce a global minimum tax of 15 percent on corporate profits.

Taken together, these “solutions” are designed to undermine the corporate tax’s connection to a physical location and make it harder for domestic policymakers to create a tax system that attracts business activity through lower taxes. The new OECD system aims to lock every country into a centralized Paris-based minimum tax rate and tax base,” Dr. Michel notes. That, he insists, would lead to higher and less efficient business taxes worldwide. In turn, Prince Michael comments: “This eliminates healthy regional competition and invites a cozy – or rather crony – global mediocrity. GIS research has predicted that such technocratic projects have all the ingredients for stunting the growth in Europe even further.”

A plan to relocate hundreds of billions of dollars in taxing rights

In his July 2023 testimony before the U.S. Congress, Dr. Michel has quoted calculations proving that Pillar One would reallocate “an estimated $130 billion to $200 billion of large multinational corporate profits to countries where customers are located. The firms affected by the minimum tax (Pillar Two) are largely U.S.-based businesses.”

A fully implemented OECD process could remove the incentive to keep corporate tax rates low and reward countries that lack innovative and entrepreneurial business sectors due to bad policy choices, the expert thereby adds.

The strong case for tax competition

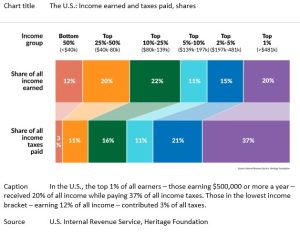

The current international tax system may be seen as imperfect, as it allows for tax planning and does not tax 100 percent of profits, Dr. Michel argues in an analysis for GIS, “The benefits of global tax games.” However, for the most part, these are features, not flaws, he maintains, thereby stressing that tax havens are crucial for international competition to attract investment through better tax systems. This rivalry has facilitated economic growth and trade, producing benefits for consumers around the world with little harm to revenue collections. “Tax competition, for example, has forced corporate tax rates among OECD countries to fall from more than 45 percent to less than 25 percent over the past three decades – while revenues have been relatively stable,” he also points out.

He thereby adds that tax optimization, so detested by the OECD, can act like a “pressure release valve” that puts a check on overly burdensome capital taxes. If these release valves would become less effective, global tax burdens will increase, slowing economic growth around the world.

34% is the average tax-to-GDP ratio in OECD countries.

👉 46% in France 🇫🇷

👉 44% in Sweden 🇸🇪

👉 43% in Italy 🇮🇹

👉 39% in Greece 🇬🇷

👉 37% in Germany 🇩🇪

👉 33% in the UK 🇬🇧

👉 26% in the U.S. 🇺🇸Read more about the push for a centralized global tax system that could lead to… pic.twitter.com/x08Jg4hPE7

— Geopolitical Intelligence Services (@GIS_Reports) October 25, 2023

Compliance: High costs and risks

Another big problem described by the publication is that the information tracking, reporting and sharing requirements that are included in the OECD’s Two-Pillar “solution” would push the already-excessive demands for reporting and globally sharing proprietary business information to new heights. That is seen to give rise to at least two significant problems.

Firstly, the requirements are exceedingly costly already. Secondly, a World Bank working paper entitled “The Dark Side of Disclosure” has described revealing financial information as a “double-edged sword”, because once firm information is disclosed, the threat of government expropriation is widespread, allowing bureaucrats to gain access to the disclosed information and use it to extract bribes.

A high-tax future

Developed countries on both sides of the Atlantic have been bullying the world into harmonizing corporate taxation, the other author of the GIS publication, Italian economist Enrico Colombatto argues, in his report on the global corporate tax debate. That would benefit high-tax welfare states that wish to escape the pressures of competition from smaller and leaner governments, he notes. Also other scholars have characterized the OECD campaign against tax competition as an effort to establish an international tax cartel.

Harmonizing corporate taxation across borders is the sure recipe for more public expenditure and slower growth, Professor Colombatto maintains, thereby predicting dire long-run effects of taxing corporate profits:

“Financial fragility will create opportunities to introduce more regulation (possibly justified by the need for more stable growth), more industrial policy (in fact, subsidies to selected companies and industries) and more tampering with labor markets, if unemployment arises.”

He thereby cautions that introducing a relatively low harmonized tax floor, at 15 percent, would serve to minimize opposition to harmonization. Once this is accepted and becomes a standard, future discussions will focus on the level, not the principle. Raising the floor will be easier, and harmonized taxation can more easily be extended to other domains, Colombatto cautions.

Global public debt was nearly $92 trillion in 2022.

That translates to around $11,500 per person.

What does per capita government debt look like in various countries?

🇺🇸$92,500

🇮🇹75,000 euros

🇩🇪37,000 eurosExperts warn that it could get worse. Read more about the consequences… pic.twitter.com/AWlmlTNJhj

— Geopolitical Intelligence Services (@GIS_Reports) October 24, 2023

However, not all is lost, as a big part of the OECD “solution” is still being negotiated.

The EU and several developed countries have adopted Pillar Two (15 percent minimum corporate tax), and international firms operating in Europe are preparing to be subject to it in 2024, but the U.S. Congress is in no mood to accept such a measure. Without the U.S. on board, the tax cannot become global.

Pillar One (redistribution of taxing rights) has met with significant resistance, as Washington and many governments worldwide display little enthusiasm for surrendering their taxing authority to some bureaucracies far away. The GIS Dossier publication this process in more detail and offers specific scenarios.

Remembering the basics

In this time of relentless pressure from income-hungry governments, it is essential to bear in mind the basics, GIS founder Prince Michael cautions. He states:

“Public administration should be at the service of citizens. Any good service organization should be lean, efficient and cost-effective. Taxes should be fair compensation for the services rendered, not a system for feeding an increasingly greedy administration and its redistribution schemes. In fact, social redistribution has degenerated to a tool used to satisfy the clientele of political parties.”

Find out more about how politicians have been replacing healthy international tax competition with a centralized scheme that set the stage for ever-higher taxes.

Buy our newest dossier: https://t.co/66fX50Ban0 pic.twitter.com/TFfQa1Zh9O

— Geopolitical Intelligence Services (@GIS_Reports) October 20, 2023